Latest Results

Latest Financial Announcements

Financial Announcements for the Current Term

- Financial Results Briefing for the Third Quarter of the Fiscal Year Ending March 31, 2025

- Financial Results Briefing for the First Half of the Fiscal Year Ending March 31, 2025

- Financial Results Briefing for the First Quarter of the Fiscal Year Ending March 31, 2025

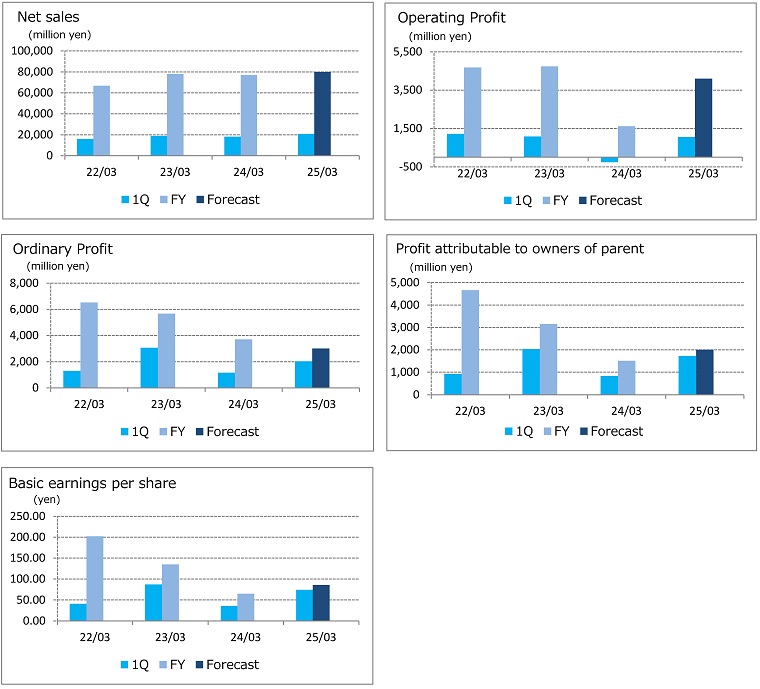

Trends in the Past Three Fiscal Years and the Current Fiscal Year

| 23/3 | 24/3 | 25/3 | 26/3* | ||

|---|---|---|---|---|---|

| Net sales (million yen) |

FY | 77,962 | 76,895 | 82,884 | TBD |

| YoY | 16.6% | (1.4%) | 7.8% | - | |

| Operating profit (million yen) |

FY | 4,739 | 1,617 | 4,226 | TBD |

| YoY | 1.2% | (65.9%) | 161.2% | - | |

| Ordinary profit (million yen) |

FY | 5,675 | 3,710 | 3,926 | TBD |

| YoY | (13.1%) | (34.6%) | 5.8% | - | |

| Profit attributable to owners of parent (million yen) |

FY | 3,147 | 1,511 | 2,227 | TBD |

| YoY | (32.5%) | (52.0%) | 47.4% | - | |

| Basic earnings per share (yen) |

FY | 135.01 | 64.86 | 95.58 | TBD |

| - | - | - | - | - | |

*The consolidated financial results forecast for the fiscal year ending March 31, 2026 has not been stated because it is difficult to make a reasonable calculation at the time of the announcement of the full-year results on May 15.

Overview of The Consolidated Financial Results for the Fiscal Year Ended March 31, 2025

Net sales in the fiscal year ended March 31, 2025 under review amounted to ¥82,884 million, an increase of 7.8% year-on-year, reflecting increased sales in the VCCS, CTC and FC/MD segments. Operation profit came in at ¥4,226 million, an increase of 161.2% year-on-year, because profit of the VCCS segment improved stabilized. Also, both CTC and FC/MD segments posted a profit increase. Ordinary profit increased by 5.8% year-on-year to ¥3,926 million, reflecting an increasing operation profit despite exchange loss of ¥352 million attributable to the strengthening of the yen. Profit attributable to owners of the parent increased by 47.4% year-on-year to ¥2,227 million reflecting the normalization of the tax rate despite the extraordinary loss of ¥223million including business restructuring cost associated with layoff in a subsidiary because of sluggish demand in the Chinese market in the second quarter of the fiscal year. Also, ¥361 million loss on disposal of fixed assets due to review of development of technical software was recorded as an extraordinary loss. The average exchange rate for the fiscal year ended March 31, 2025 was ¥152.60 against the US dollar (¥144.58 in the previous fiscal year), while the closing rate was ¥149.52 against the US dollar (¥151.41 in the previous fiscal year).

Overview of Financial Results for Each Segments and Explanation of Consolidated Results Forecast

VCCS (Core product: Antenna for Vehicle)

In the automotive market, the main market for this segment, demand for new vehicles is slowing in response to the global economic slowdown, although sales are on an improving trend driven by a stable semiconductors and component supply. A breakdown by region shows that sales in the United States, China, and Japan were flat.

In these circumstances, mainstay products for automobile manufacturers, such as shark fin antennas and GPS antennas, slightly decreased year-on-year because of a slump in sales of Japanese automobile manufacturers to the Chinese market and an impact of production adjustments by some customers despite higher sales in Japan.

As a result, sales for this segment were at the same level as the previous fiscal year to ¥55,961 million (up 0.7% year-on-year). The segment reported the profit of ¥2,838 million (down 8.4% year-on-year), due in part to increase in shipping and other logistics costs and higher labor costs at production bases in China and Vietnam associated with the strengthening of the local currencies, despite improved production efficiency through the review of production system and stable receipt of orders.

CTC (Core Product: Semiconductor Testing Socket and Probe Card)

In the semiconductor testing market, the main market for this segment, slightly increased year-on-year due to strong demand for testers related to generative AI. However, demand for PCs and smartphones remained still stagnant, and demand growth for industrial machinery and automobiles was slowing.

In these circumstances, sales of jigs for semiconductor back-end testing, the mainstay product of the Group, increased year-on-year, due to capturing demand for testers related to generative AI despite a decrease in orders for logic semiconductor testing sockets. Sales of jigs for semiconductor front-end testing increased year-on-year because of turning upward sales after the second half of the fiscal year in MEMS probe cards (YPX) for high-frequency electronics components testing and increased sales in the turnkey business which offers one-stop solutions services including peripheral devices.

As a result, sales for this segment increased year-on-year to ¥15,614 million (up 24.1% year-on-year). The segment reported a profit of ¥1,479 million (a loss of ¥794 million in the previous fiscal year), due to increased profit associated with an increase in sales and improved product mix despite temporary technical issue response costs.

FC (Core Product: Fine spring connector for electronics) ・MD (Core Product: Medical devices and units)

In the market for mobile communication terminals, a key market for this segment, sales of wearable terminals are expected to grow given their diversification and greater sophistication, and unit shipments of smartphones were increased year-on-year. Demand for POS terminal market has been growing steadily in a wide range of industries, including those engaging in logistics and manufacturing, with a view toward improvements in operational efficiency through information management.

In these circumstances, sales for FC business, for which fine spring connectors act as core products, increased year-on-year, reflecting a recovery of orders received of the POS terminals due in part to resolution of the end of customers' production adjustment and continued solid sales of wearable devices such as wireless earbuds.

In the MD business, sales increased year-on-year due to strong sales of both unit products and catheter components for a major domestic medical device manufacturer, which is a major customer. In addition, sales for the venture ecosystem in which the Company participates as a manufacturing partner remained solid.

As a result, sales for this segment increased year-on-year, to ¥11,032 million (up 31.8% year-on-year). The segment reported a profit of ¥789 million (up 571.8% year-on-year) chiefly owing to increased profit associated with an increase in sales in FC business.

Incubation Center (Core Product: Antenna and providing solutions for MaaS/IoT)

The Company has been engaged in full-scale business development efforts, aiming to create new businesses and innovate business models for new growth markets such as MaaS, and IoT as well as the optical communication market for higher-speed and larger-capacity communication. The MaaS/IoT market, which is a key market for this segment, is expected to grow steadily, reflecting the advance of mobility including car sharing, and the widespread adoption of IoT connecting everything through the Internet.

In these circumstances, Platform business has made progress in expanding sales of MIMO antennas utilizing smart antenna technologies for IoT, and vehicle key management solutions for MaaS and rental cars.

For Advanced Device business, which included the segment, the Company had developed systems for the mass production of optical connector products utilizing photoelectric conversion device technologies for the optical communications market. However, the Company disbanded developmentally this business in the second quarter as a photoelectric conversion project for the semiconductor testing market.

As a result, sales for this segment decreased year-on-year, to ¥271 million (down 21.7% year-on-year). The segment reported a loss of ¥886 million (a loss of ¥811 million in the previous fiscal year), because the segment, which is in the early stages of its development, generates sales at a small scale and involves up-front investment.

Future Outlook

The forecasts for the fiscal year ending March 31, 2026 have not been determined at this point in time due to the extremely large number of uncertain factors such as the US tariff policy and the price negotiations in response to it, and will be disclosed as soon as a reasonable calculation can be made.

For the fiscal year ending March 31, 2026, the Company expects to pay a dividend of ¥48 per share (an interim dividend of ¥24 and a year-end dividend of ¥24), the same amount as for the fiscal year ended March 31, 2025, based on the amount obtained by multiplying the amount of net assets as of the end of March 31, 2025 by 2.2%, in accordance with the profit distribution policy for shareholders (DOE: 2.2% as a guideline).